Eldon Neighbor is an independent insurance agent in eastern Iowa. Last year his own carrier left the state and dropped his coverage. "Instead of doing what they're supposed to do, which is serve their customers, they are cutting them loose by the droves," he told the New York Times. An insurance agent who can't get insured. If you wanted to understand the American property insurance market in one detail, there it is.

He's got plenty of company. At least four carriers have pulled out of Iowa, dumping tens of thousands of policyholders. In Cedar Rapids, Dave Langston spent months trying to find anyone willing to insure his HOA's townhouses. Over in Iowa City, Dylan Nice spent $4,000 trimming a silver maple so Travelers could photograph his roof from a satellite. They dropped him anyway.

The weather is real enough. Iowa hail events jumped 133% between 2022 and 2023. The state set a tornado record in 2024 with 122. The August 2020 derecho alone generated over 200,000 claims and $11 billion in damages still sitting on the books. For every dollar Iowa insurers collected in homeowner premiums in 2023, they paid out $1.44. Minnesota was worse: in 2022, companies paid out $1.92 for every dollar in.

So premiums climb. Iowa saw 14% in 2024 with 19% projected for 2025. A study in npj Climate Action documented increases up to 50% in Iowa, Arkansas, and Utah. Freddie Mac found national premiums jumped 57% from 2019 to 2024. The Consumer Federation of America calculated that American homeowners spent $21 billion more on insurance in 2024 than they did in 2021. Joan Hasper, in Minnesota, watched her condominium HOA fees double past $1,100 a month after nearly all major insurers abandoned the master-policy market. "The last year has been hell, to be honest with you," she said.

Bill Montgomery, CEO of Celina Insurance Group, one of the companies that left Iowa, offered a sentence worth carving in stone:

"Climate change is real. We can't raise rates fast enough or high enough."

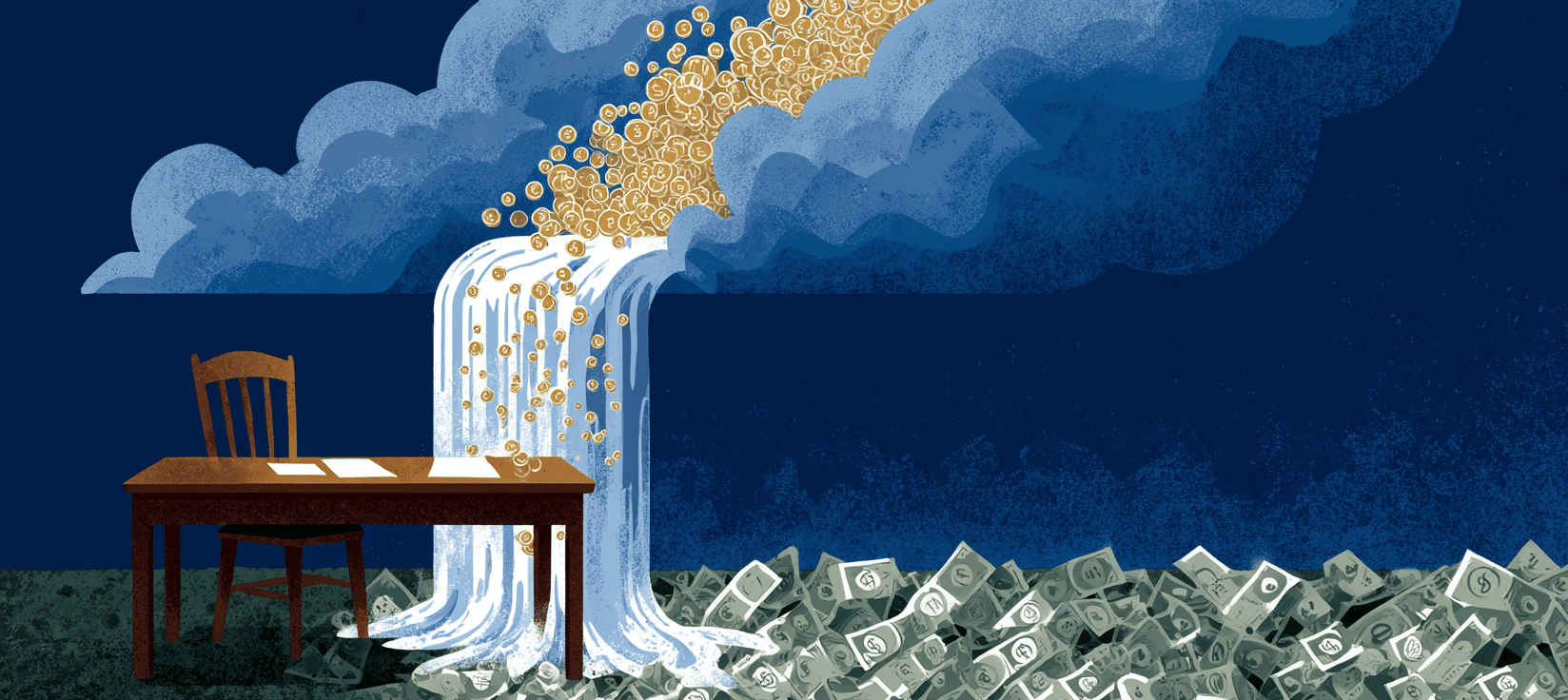

So the insurance business is bleeding money. Meanwhile, the business of insuring the insurance business is having the best years of its life.

Where the Money Went

Total dedicated reinsurance capital hit a projected $838 billion by the end of 2025. At January 2026 renewals, property catastrophe reinsurance rates fell 12% to 15%. Catastrophe bond issuance hit $25.6 billion, smashing the prior record by 45%. Reinsurers posted returns on equity north of 17%. Capital is flooding in because the returns are spectacular.

Iowa's insurance commissioner, Doug Ommen, explained it plainly: "It's the reinsurers that have made it much more difficult for these mid-size, smaller companies to get reinsurance."

After heavy losses in 2022–2023, reinsurers raised the threshold at which their coverage kicks in. Everything below that line, the primary insurer eats alone.

It amounts to raising the deductible on your insurer's own insurance policy. Hurricanes punch through high thresholds in a single event. Hailstorms and derechos don't. They are frequent, widespread, and individually smaller. They accumulate beneath the attachment point where reinsurers never feel them. Gallagher Re noted that insured catastrophe losses exceeded $120 billion for the sixth straight year, but "limited loss flow into reinsurance reflected higher attachment points." The losses happened. They just didn't flow up. Munich Re's 2025 figures put it starkly: non-peak perils, the category that includes hail and severe convective storms, drove $166 billion in total losses globally, roughly $98 billion of it insured. That exceeded hurricane losses for the year. Hail, wind, tornadoes, derechos. The unglamorous stuff. It now costs more than the named storms that lead the evening news.

Severe convective storm losses in the U.S. alone hit $54 billion in 2024, well past the $33 billion annual average since 2015. Insurance executives ranked these storms as their top concern for annual earnings after reinsurance recoveries, with 87% expressing significant concern over future SCS losses.

And while the price goes up, the coverage shrinks. The Federal Reserve Bank of Minneapolis found insurers quietly converting flat hail deductibles into percentage-based ones. On a $350,000 home, that's $7,000 out of pocket instead of $1,500. You pay more for the privilege of covering more of the damage yourself.

Buried in all of this is a finding most people will never encounter: climate models have been systematically underestimating warming because industrial pollution was acting as an inadvertent sunshade. As that pollution declines, the models get more wrong.

Eldon Neighbor, the insurance agent in eastern Iowa who can't insure his own house, might describe this arrangement differently. But nobody in the capital markets is asking him.

Things to follow up on...

-

Industry lobbies against regulation: An InfluenceMap report released this week found major insurance groups actively lobbied against international climate risk guidance, with the U.S. Chamber of Commerce questioning whether climate change poses financial stability risk to the sector even as homeowner cancellations hit nearly two million policies in five years.

-

The flood maps miss floods: A February 2026 Willis Towers Watson analysis documents that FEMA flood maps do not account for pluvial flooding, the rainfall-driven kind that swamps basements far from any river, leaving homeowners in "safe" zones uninsured for the water that actually hits them.

-

Zillow pulled climate scores: After launching climate risk data on listings in September 2024, Zillow quietly removed the information following industry complaints that it was hurting home sales, even as First Street estimates climate-driven warming could erase $1.47 trillion in real estate value over three decades.

-

One in thirteen is uninsured: The Consumer Federation of America found that one in thirteen American homeowners now carries no insurance at all, leaving an estimated $1.6 trillion in property value unprotected as premiums push coverage out of reach.