The actuary's fingers are cold when she opens the rate model Tuesday morning. Not from temperature—the office is climate-controlled to exactly 71 degrees—but from what the spreadsheet is about to make her do.

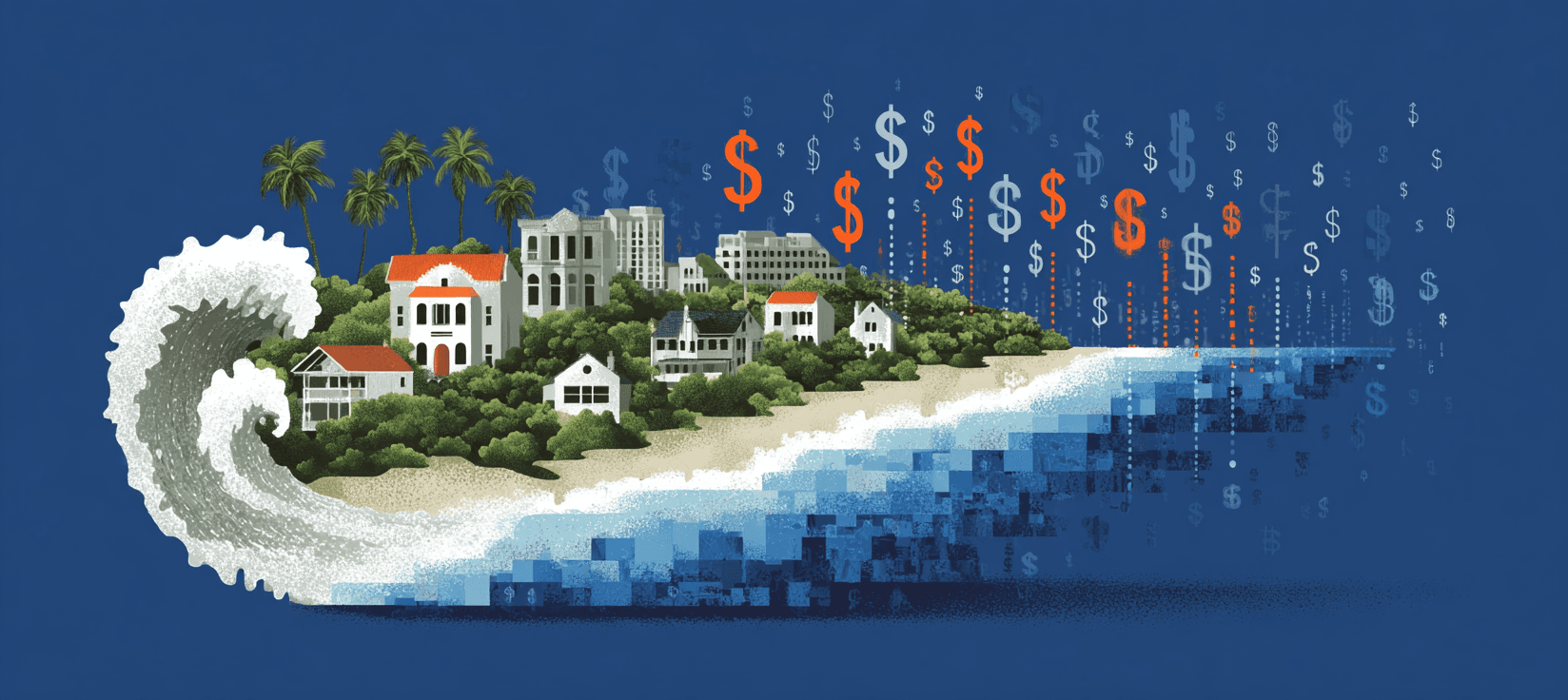

She's been assigned Portfolio Rebalancing, Southeast Region, which is insurance industry language for: figure out how to keep selling policies in Florida without losing money. The company lost $847 million in catastrophic claims last year. Her job is to make that number smaller without actually leaving Florida, which the executives have determined would be "optically challenging."

She types the first variable: Florida rate cap, 10% maximum annual increase per state regulation. The pressure starts behind her sternum. The actuarially sound rate would be 34% higher. That 24-point gap has to come from somewhere.

The model suggests Virginia.

Three months ago, she sat in a conference room watching her manager present a Florida rate increase to the state insurance commissioner. The numbers were clean: hurricane exposure up 40%, claims costs up 35%, requested increase 34%. The commissioner's face didn't change. "Denied. Maximum allowable increase is 10%."

Her manager's jaw tightened. The actuary felt her throat constrict—not surprise, but recognition. She'd seen this before. California denying wildfire increases. Texas capping hail damage adjustments. States with the highest climate exposure maintaining the lowest rate growth.

Back at her desk, she'd opened the Virginia model. Her pulse was visible in her wrists. The algorithm was already suggesting it: redistribute the denied Florida increase across low-friction states. Virginia's insurance commissioner would approve 50.8% without headlines. Nebraska would take 38.3%. Montana would take 44.1%. The math was elegant. The math was legal.

She'd clicked Calculate and watched $3.2 billion in climate risk flow from high-friction states to low-friction states. From places with strong insurance commissioners to places where regulators assumed rate increases reflected local conditions. From people who chose ocean views to people who chose safety.

Her mouth tasted metallic. It still does, typing the same variables again.

Last week, she read a Federal Reserve working paper during lunch. The language was academic, clinical:

"households in low friction states are disproportionately bearing the risks of households in high friction states."

She recognized the pattern immediately. The researchers had quantified what her model did automatically—identified regulatory arbitrage opportunities, optimized risk distribution across jurisdictions, transformed geography into financial liability.

Her sandwich sat untouched. The paper estimated that if all states had similar regulations, rates in strictly regulated states would have grown 20% faster. That missing 20% was flowing through her spreadsheet right now. Virginia absorbing Florida's hurricanes. Pennsylvania absorbing California's wildfires. New Hampshire absorbing Texas's hail damage.

She'd closed the paper. Her hands had gone numb at the fingertips. They haven't quite recovered.

Her manager reviews the portfolio rebalancing in the afternoon. He's pleased. The model works. Florida stays profitable. Virginia absorbs the difference. By 2024, 95% of all US ZIP codes experienced premium increases over three years, averaging 24%.

"Any concerns?" he asks.

The actuary thinks about a woman in Charlottesville opening her renewal notice. The way her hands will go cold. The way her body will understand before her mind does that she's being charged for someone else's hurricane. The way she'll call customer service and hear "market conditions" and know it means nothing and everything.

"No concerns," the actuary says. Her voice sounds normal. Professional.

That evening, her own insurance renewal arrives. She lives in Ohio, deliberately inland, deliberately nowhere near any coast. Her premium increased 18%. She stares at the number. Her diaphragm won't expand properly.

She knows exactly why this happened. She built the model. She optimized the distribution. She made Ohio pay for Florida because Florida's regulator wouldn't let Florida pay for Florida.

The letter says "market conditions." It doesn't say "regulatory arbitrage." It doesn't say "your actuary's optimization algorithm." It doesn't say "you're subsidizing someone's beachfront property because their state commissioner protects them and yours doesn't."

She writes the check. Her hand cramps around the pen. Somewhere in Florida, someone's premium stays artificially low. Somewhere in her office, her model balances. Somewhere in a state capital, a regulator denies another rate increase, and the system compensates by finding someone else to charge.

Tomorrow she'll optimize the Midwest portfolio. Tomorrow she'll redistribute more climate risk from people who chose disaster to people who didn't.

Her fingers are cold again. They've been cold since she opened that first Florida file. The spreadsheet keeps them that way.

Things to follow up on...

-

New Hampshire's modest increases: While disaster-prone states see double-digit premium hikes, New Hampshire homeowners face only a projected 3% increase in 2025, making it one of the few states where the cross-subsidization pattern seems to break down.

-

Industry profitability returns: After years of losses, most major insurance carriers achieved profitability by mid-2024, raising questions about whether rate increases will moderate or continue despite improved financial performance.

-

Uninsured homeowners rising: Seven percent of homeowners now lack insurance entirely, with 43% citing affordability as the primary reason, suggesting the cross-subsidization system is pricing some people out of coverage altogether.

-

Construction cost inflation: Building material and labor costs increased 35-40% between 2020 and 2024, roughly twice the pace of general consumer inflation, creating additional upward pressure on premiums independent of climate risk redistribution.